China’s “New Cities” share a few defining qualities. They are master-planned, designed specifically to increase and diversity the tax base of industrial districts, attract FDI, and foster growth in higher-value tertiary industries. Local governments may institute policy incentives for new company registration and often relocate government headquarters to the area, thus prompting SOEs to buy or lease large quantities of nearby office space.

Several new cities, separated from the traditional CBDs by geography and policy, have already begun to exert pressure on the office market, redefining city maps and drawing into question the distinction between core and non-core markets.

Using Tableau data visualization software, we have selected several examples from across China to demonstrate the recent performance and rapid growth of such areas.

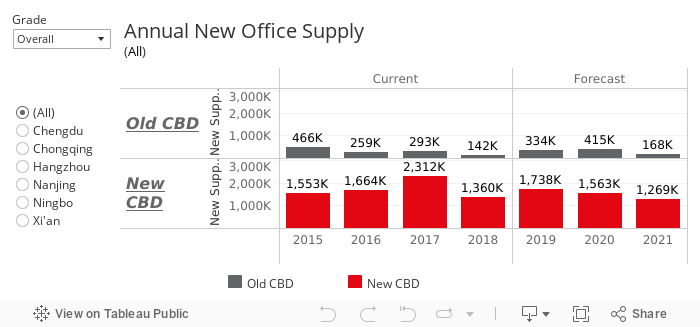

New cities have seen the lion’s share of recent office development in China. Across our six example cities, overall construction in new cities was more than 6 times that in old CBDs between 2015 and 2018. In terms of performance, two new CBD’s stand out – Hangzhou and Chengdu.

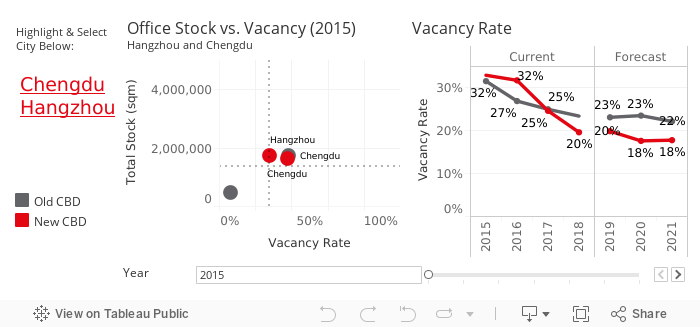

Qianjiang New City (QJNC), Hangzhou’s New City, did not see its supply peak until 2018, by which point its mature transport infrastructure and newer, higher-spec office buildings led it to supplant the old CBD, Huanglong, as the primary destination for finance and professional services firms. Huanglong, by contrast, is primarily populated by older Grade B office buildings. You can explore this yourself by selecting Hangzhou in the tool below: Vacancy in QJNC fell from 13 percentage points between 2015 and 2018.

One similar example is Chengdu’s Financial City in the South CBD. Over the last few years, affordable rents and favourable policies have successfully populated Financial City with West China headquarters representing a variety of sectors. Vacancy similarly from 39% in 2016 to 25% in 2018, challenging the traditional CBD.

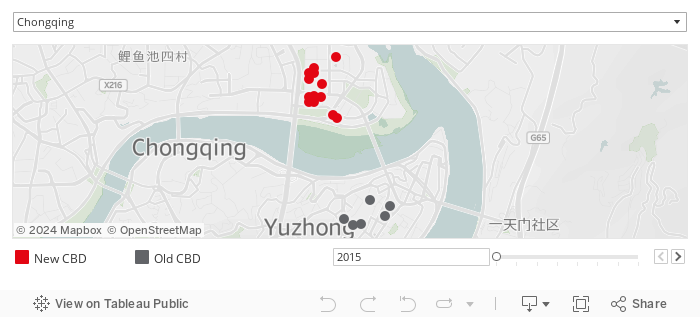

Other new cities are defined less by performance and more by supply booms. Chongqing’s old and new CBDs provide us with a sharp visual dichotomy. Jiefangbei, the city’s traditional office cluster, has been undermined by excessive tourist traffic and aging buildings. To facilitate urban renewal, Jiangbeizui was established in 2010 just across the river. Since then, Jiangbeizui was accounted for more than 42% of the Grade A office construction in Chongqing, three times more than Jiefangbei. This construction boom can be seen using the time slider below.

We can also use the map above to display the growth of two more new cities: Nanjing’s Hexi New District and Ningbo’s Eastern New Town. Both areas exemplify local-government-led development projects whereby SOEs function as anchor tenants. In the case of Nanjing, you can see Hexi’s centre of gravity begin to shift south after 2017, when a government-backed developer completed ten Grade A office towers housing state-owned banks, insurance and securities companies.

Across the country, the path forward is clear. New cities will continue to attract or command development, shifting market dynamics and reshaping the office market.

For more information on China’s property market, including custom dashboards, please contact REISChina.Technology@ap.jll.com

More on 'Office' in 'China'

- Emerging industries fuel Guangzhou’s office leasing demandJanuary 13, 2026

- Evolving demand drives Shanghai’s office leasing momentumDecember 5, 2025

- Nanjing’s new frontier: tech shapes the next-gen workplaceOctober 31, 2025

- China’s cross-border e-commerce companies fuel office demandSeptember 30, 2025

- Decoding Shanghai office tenants’ CRE strategiesJuly 11, 2025